Excise Duty and Surtax are taxes charged, levied and collected in respect of goods which are imported into or are manufactured or produced within Zimbabwe.

On what goods is Excise Duty levied?

- Manufactured cigarette tobacco, Cigarettes, cigars cigarillos

- Any potable liquid containing more than 1.7% of absolute alcohol. Except honey beer or opaque beer which is not designated opaque beer

- Aerated beverages (e.g., soda water and energy drink)

- Hydrocarbon oils such as petrol, diesel, and paraffin

- Air time

On what goods is Special Surtax on beverages Sugar content levied?

- Beverages containing added sugar

Licensing

- In order for any person to manufacture any of the goods liable to excise or surtax, he/she must apply to the Commissioner of Customs & Excise, for a license and the license issued or renewed, expire on the 31st December in the year in respect of which it was issued, (except airtime operators). However, any person may produce without a license and without payment of duty for domestic use but not for sale or dispose for profit to any other person.

Who applies for license?

Any person manufacturing any excisable goods

Registration requirements

- Proof of address e.g., a recent electricity or water bill and copy of ownership of the premises.

- If leasing, copy of the lease agreement which shows the owner of the building and the lease period which should not be less than 12 months.

- Copy of Identification of Directors and key management and their proof of residence

- Copies of police clearance for directors and key management

- Current bank statement.

- Valid tax clearance certificate

- Attach your business plan.

- Certificate of Incorporation, C.R. 6 and C.R. 14; from the Registrar of Companies

- Copies of Health Certificates from Ministry of Health and or City Council Health Department. If the raw materials or final products are flammable, submit an inspection report/ certificate from City/Municipal Fire Department.

- Estimated Sales projections for each product per year for 3 years showing projected output (USD); excise duty/year)

NB: An inspection will be carried out to verify the application. Applicant will be required to enter into bond guaranteed by a registered commercial bank or insurance company before a licence is issued.

How to apply

Log into Self Service Portal (SSP) in TaRMS

- Select the appropriate TIN to be registered.

- Go to “Tax Payer Information” tab

- Click “Tax Type”

- Click “New Tax Type”

- Select “Excise Duty” and click “Open”

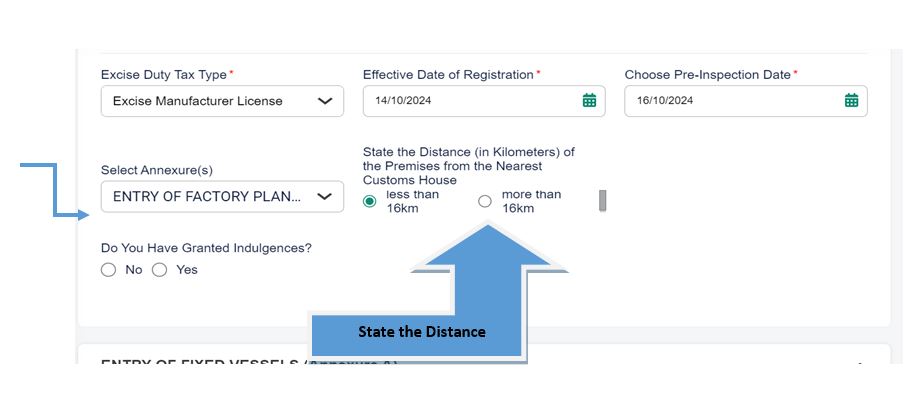

- Click on the “Excise Duty Tax Type” drop down menu and select “Tax type”

- Click on the “Effective Date of Registration” and enter the respective date.

- Click on the “Choose Pre- inspection date” and select the inspection date

- Click on the “Select Annexure(S)” drop down menu and select all annexures

- Choose the distance of the premise by clicking on the “State the distance (in Kilometres) of the Premises from the nearest customs

House”

|

- Choose whether or not there are any granted indulgence by selecting “Yes / No”

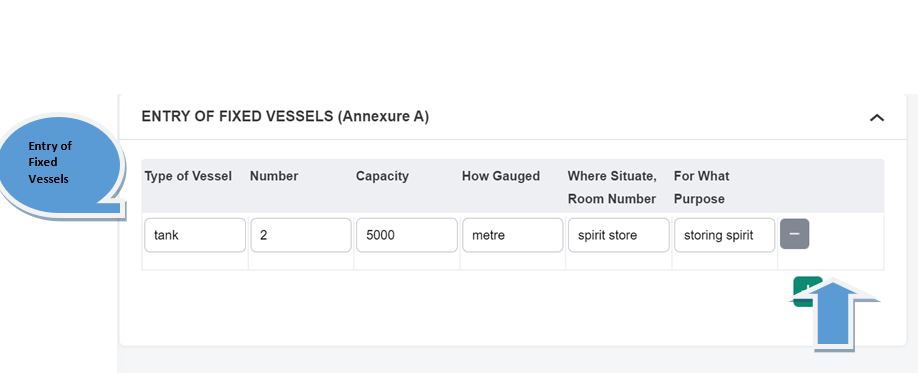

- Click “Entry of Fixed Vessels (Annexures A)”

|

- Click the (+) Tab to add more vessels or click the (-) Tab to remove a vessel.

- The above applies to “Annexures B and C”

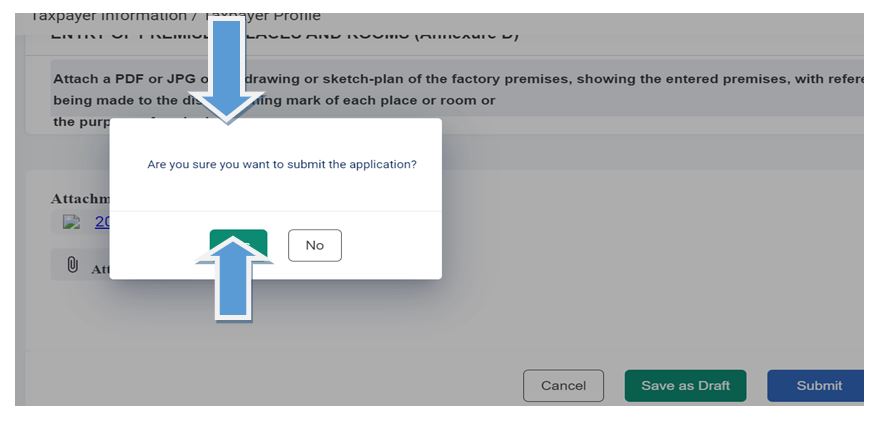

- Proceed to “Annexure D” and attach the ‘SKETCH MAP” in acceptable format (Pdf, jpeg) and Click “Submit”

- A pop up message will prompt you to complete the process by selecting ‘YES’ will appear.

|

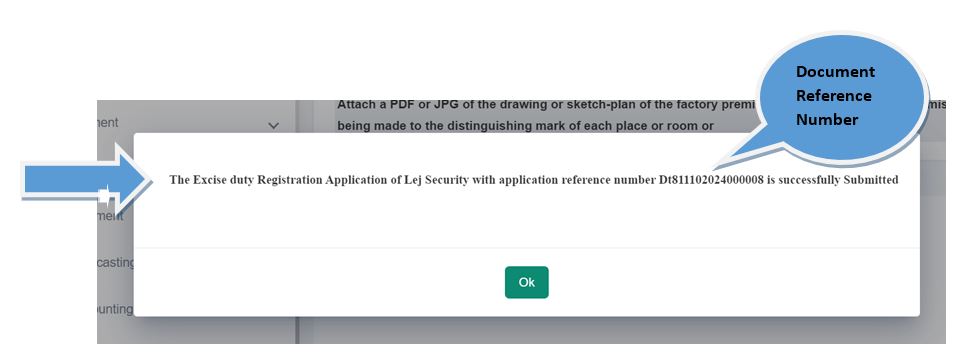

- A pop message will appear with “DRN if successfully submitted”

|

- The application is sent to ZIMRA for review and approval if all conditions are met and upon approval of the application, a notification is issued to that effect.

N.B. Before any licence is issued, you shall enter into a bond. ZIMRA reserves the right to reject bonds which have insufficient penal sum.

Bond Application

- Attach a Resolution of the Board of Directors appointing a Principal Officer as well as agreed amount of Excise Manufacturer’s and/or Spirit Rebate bond. If the goods to be manufactured will be sold in mostly foreign currency, the bond penal sum should be in foreign currency.

- Bond cover letter from the surety

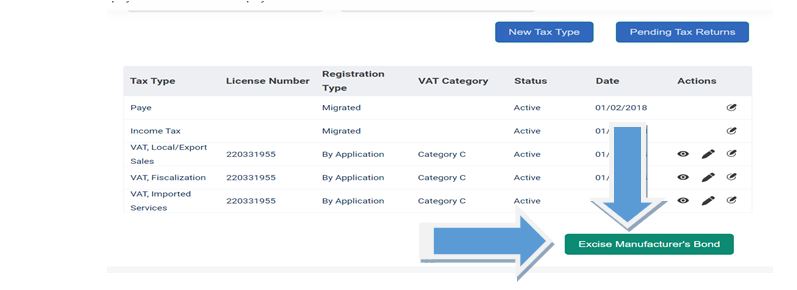

SSP Bond Registration Menu Path in TaRMS

- Go to Taxpayer Information

- Click “Excise Manufacturer’s Bond under Tax Type” or Spirit Rebate bond whichever is applicable

|

- The Excise Manufacturer’s form will appear.

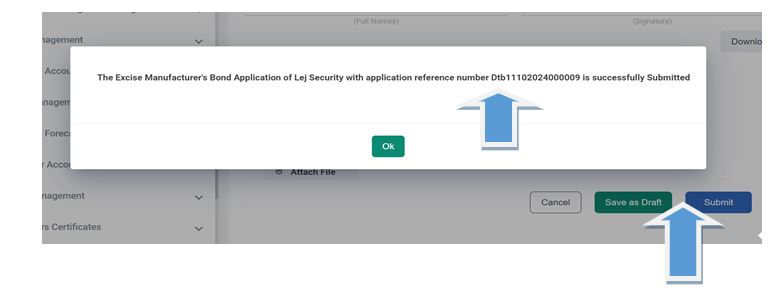

- Complete and download form to enable bond insurer to sign and have forms endorsed by ZIMRA

- Attach signed form and click on submit icon.

- A pop up screen to submit the application will appear.

- A pop message with DRN will appear if successfully submitted.

|

Excise Manufacturer Licensing Instruction

- Upon successful registration as an Excise Manufacturer or Spirit Rebate user, an automated assessment for the payment of license fees will be generated.

- License fee payments will be processed if the single account is sufficiently funded.

- A valid license will be displayed in the General Information Tab for the specified calendar year.

Right to appeal

Any person whose application has been rejected or whose license has been revoked has the right to appeal.

Refusal, Suspension and Cancellation of Licence

The Commissioner of Customs & Excise has a discretion to refuse to renew, suspend or cancel the licence of any person for any of the following reasons:

- Has contravened any provisions of the Act or has failed to comply with any rule made by the Commissioner.

- If a licensee fails to comply with the requirements of the law, or fails to carry out any duty imposed by the Act with respect to his premises or any buildings, appliances, stock book or the mode of conducting his business.

Offences

The following are some of the major offences which one can commit:

- Manufacture any goods liable to excise duty or surtax without a license or lawful authority or have in his possession or custody or control any manufactured or partially manufactured goods liable to excise duty

- Failure to keep books as required by the Act, or fails to make entry in such books, erases or obliterates any entry or destroys or makes away with such books

- Refuses to allow an officer at any time to inspect the books

- Submits a false return

- Neglects or refuses to give such information as to his operation in the manufacture of goods liable for excise

- Found without lawful excuse in any place where the illegal manufacture of goods liable to excise duty or surtax is being carried out